But between now and then, I hope to get one post out a month to keep my typing fingers in shape, as well as these monthly updates.

Read on intrepid followers, for the dazzling numbers that made up February...

I'd rather go for the higher end of the scale though, so to fund my $30,000 lifestyle in retirement, I'm going to need to find $750,000 in the next eight and a half years, in accordance with the four percent rule.

The investment plan

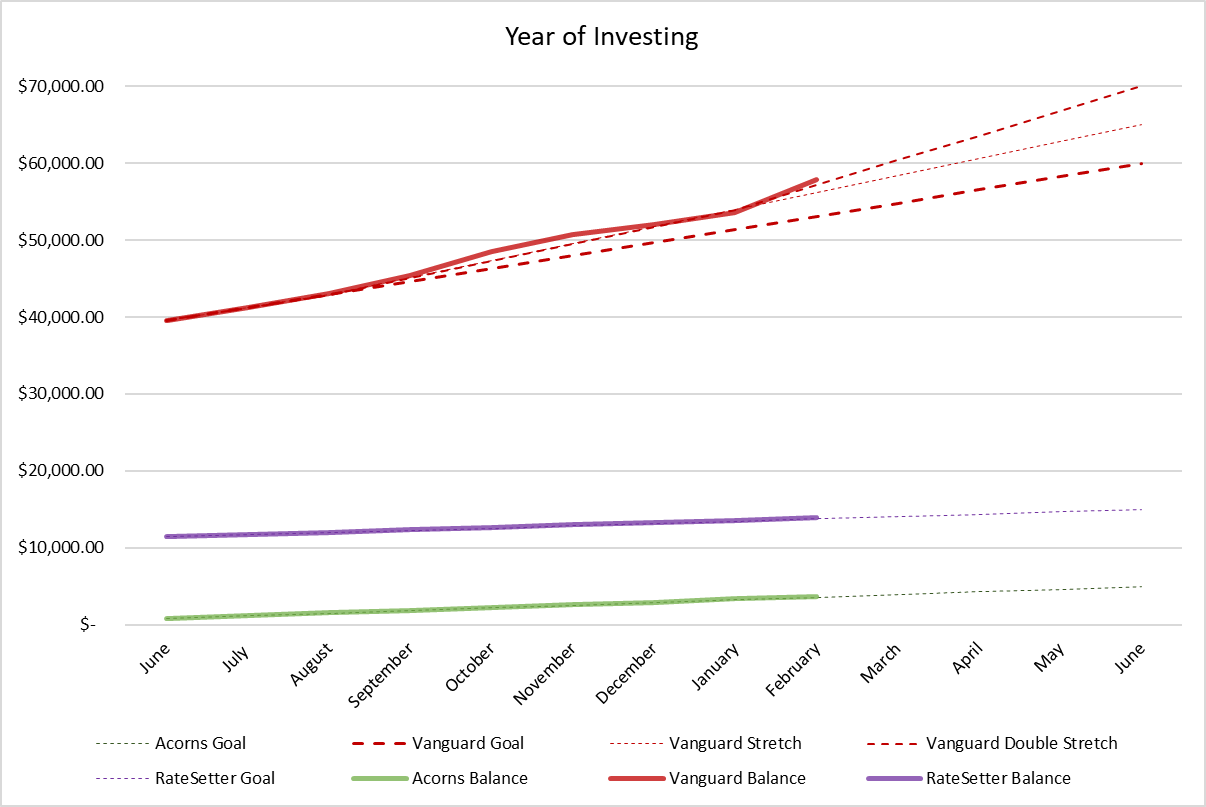

For the next twelve months (July 2017 - June 2018) I am going to focus on supercharging my investments. The earlier in my retirement journey I start investing the more heavy lifting will be done by compound interest. By spending my money on buying more money in the early years, I hope to see my investments growing on their own through the next few years.In the Year of Investing I plan on building up my existing accounts until I have just over 10% of my retirement fund. Starting from $52,000 I'm aiming for $80,000 by July 1 2018, an increase of $28,000 - just shy of $2,400 a month.

Except, not really, because I have a stretch goal, and now a double stretch! Overall I plan to have $90k invested, for an increase of $38,000, or just over $3,150 a month.

Acorns

Want to try out Acorns? Check out my review first.

February

Opening Balance: $3,415.15Deposited: $310.46

Dividends: $0.19

Market Gains: -$10.97

Current Balance: $3,714.83

Since starting The Year of Investing

Opening Balance: $813.53Deposited: $2,692.58

Dividends: $46.03

Market Gains: $162.69

Current Balance: $3,714.83

Nothing overly exciting, but that market correction at the start of February gave my portfolio a good solid kicking that it didn't entirely recover from. Still on track though.

Goal: $5,000

Amount remaining: $1,285.17 ($321.29 per month)

Current investment plan: $75 per week

Vanguard

Want to try out Vanguard? Check out my review first.

January

Opening Balance: $53,528.92Deposited: $3,650

Dividends: $0

Market Gains: $630.02

Current Balance: $57,808.94

Since starting The Year of Investing

Opening Balance: $39,566.66Deposited: $15,650

Dividends: $1,061.23

Market Gains: $1,531.05

Current Balance: $57,808.94

So my Vanguard portfolio also took a good kicking from the market correction at the start of February, but as soon as I saw the drop I threw money into my account. I figured if this was the start of a big drop, nothing in my plan would change (I've got 8 years) but if it was just a little blip I wanted to capitalise on it, and I did! The markets aren't quite back to where they were at the end of January, but they've definitely recovered, and I got in on that ride.

In fact, I did so well that I stretched my stretch goal. I'm not sure if this is ruining the power of Dollar Value Averaging, but I've got money sitting there that I really wanted to put to work.

Goal: $60,000In fact, I did so well that I stretched my stretch goal. I'm not sure if this is ruining the power of Dollar Value Averaging, but I've got money sitting there that I really wanted to put to work.

Amount remaining: $2,191.06 ($547.76 per month)

Stretch Goal: $65,000

Stretch amount remaining: $7,191.06 ($1,797.76 per month)

Double Stretch Goal: $70,000

Double stretch amount remaining: $12,191.06 ($3,047.76 per month)

Current investment plan: $1,900 per month, plus whatever extra I can find

RateSetter

Want to try out RateSetter? Check out my review first.

January

Opening Balance: $13,617.57Deposited: $200.00

Loan Returns: $97.49

Current Balance: $13,915.06

Since starting The Year of Investing

Opening Balance: $11,416.13Deposited: $1,750

Loan Returns: $748.93

Current Balance: $13,915.06

Nothing super exciting here. This is on track to hit target without me adjusting my plans at all. However the sign-up bonuses are going again. If you want a 9% return and $75 to get you started, give it a go.

Amount remaining: $1,382.43 ($276.49 per month)

Current investment plan: $200 per month

The big picture - my savings rate

In total I'm hoping to invest $23,000 during the Year of Investing (now $33,000 with my double stretch goal!). On top of that I plan to keep up with my mortgage repayments, which should see my debts drop by approximately $12,500. This means saving $35,500, (45,500) just shy of 50% of my income (just over 57%).So on top of paying down my mortgage and investing, I plan to squirrel away a little bit more so I can declare that I saved 50% of my income. In the previous 12 months I saved 41% of my income, so this year I though 'What the heck, let's push for 50%'.

According to the networthify early retirement calculator, if I pull this off I'll be able to retire in 9 years - just a few short months after my goal. A lot can happen in nine years, and I intend to prove that calculator wrong ;)

According to the Mad Fientist Lab, after February I'm only 7 years and 5 months away - that's seven months ahead of schedule!

Here's how my savings look for February:

So I bet you're wondering why February has been such an amazing month? Two simple words - Tax Return. Yes, it's true and I'm ashamed to admit it, I finally did my 2016-17 taxes in February 2018. Ouch. Thankfully it was a nice return, and I funnelled it straight into my investments.

Expenses

For the sake of curiosity, here's what I spent in February.

| Category | Spent | Budgeted | 12 Month Average |

|---|---|---|---|

| Home | $1,338.16 | $1,312.50 | $1,288.97 (down $46.75) |

| Guys. I DIY'd something! Okay it was only an $11 tap fitting but there was a lot of swearing involved and it changed my showers from a dribble of tepid sadness to a waterfall of heaven! I am so proud of me right now. Apart from that, I also paid some bills... woo... | |||

| Investment Property | $779.39 | $1,166.67 | $1,136.13 (down $68.07) |

| Literally just the mortgage. What a nice month. I made more than I spent :) | |||

| Personal Bills | $146.91 | $147.08 | $146.38 (up $0.52) |

| The usual | |||

| Groceries | $153.26 | $200.00 | $179.59 (down $5.44) |

| With My. FIRE away for half the month, this should have been a cheap month, but normally he buys the meat. I was doing really well until I decided to stock up, and suddenly $60 disappeared. | |||

| Pets | $0.00 | $29.00 | $25.30 (down $5.91) |

| Ummm, apparently I didn't buy anything? I guess my food stocks made it through a month. I did go cat food shopping this weekend though, so we only just scraped through February on a no-spend. | |||

| Roller Derby | $124.16 | $150.00 | $197.05 (down $4.06) $197.05 |

| I'm honestly surprised this isn't more. I planned to replace a lot of my gear, but ended up only buying one thing. In March I'm buying at least two items of clothing, paying accomodations for an interstate trip, and I'll actually be interstate. So yeah, March will be even more over budget. I'm not sure why I even pretend $150 a month is enough. Optimisim I guess | |||

| Travelling | $0 | $100.00 | $0.00 (no change) |

| None. I really should. Now taking suggestions - where in the world should Lady FIRE go? | |||

| Other | $429.51 | $157.25 | $191.97 (up $5.94) |

| Umm, yeah, look I have no excuses here. I drank a fair bit in the warm weather, stocked up on spirits, bought new earphones, some books, some games, I went out to lunch with my work mates... it was just one of those months. I even bought my friend a tank of petrol because she's the one who picks me up for most derby social events. | |||

| Total | $2,971.39 | $3,329.17 | $3,202.19 (down $123.77) |

| Yo my average spend is UNDER my budgeted spend! Heckin' what! This actually happen last month by a couple of dollars but I didn't notice. Now i's under by more than $100!! Yuss! An according to the Mad Fientist Lab, my early retirement date is EIGHT MONTHS ahead of schedule. This is ALL CAPS kind of excitement!! | |||

Blast from the Past!

The Year of Investing started July 2017. You can see past reports here:

This comment has been removed by the author.

ReplyDeleteThanks for the post. Have you analysed the after fees rate of return of each investment type? Have you thought of closing the Acorns and moving all to Vanguard (to save on fees?)

ReplyDeleteI've done a rough comparison and once I get the Acorns account up to $5k (end of the tax year) the fee's aren't as brutal. I opened the account because I had a bit of FOMO since everyone else had one. There is a good chance I'll close it one day, but nothing definite in the plans.

DeleteLooks like great progress on the investing, well done. The years will fly by in no time.

ReplyDeleteThanks - I'm trying to remember to enjoy myself in the meantime, but that goal is just so shiny :)

Deletethis is a sound of someone who doesn t have kids ;-)))

ReplyDeleteare your future plans taking this into account? we re close my fire date is in less than 8 years too

Ahh kid free bliss :) You're definitely right there!

DeleteI have no future plans about changing my finances for kids, because I have no future plans to have kids. I have future plans to have lots of dogs, but that's about it :)